[Estimated read time: 5 minutes]

Seven Ways to Paying Off Your Mortgage Early

Owning your home 'free and clear' is a homeowner's American dream. Some may argue that eliminating this debt, at a faster pace, may not exactly be the best use of your money. Depending on your stand, there are still a lot of homeowners that would love to be cut loose from this monthly debt.

Slow and steady will get the job done but if you just bought your home, thirty years is a long time to wait! A lot of new homebuyers looking for Oldham County real estate love the idea of owning a home free and clear. Below we will cover seven tips on how to pay off a mortgage early.

1. Round Up Your Monthly Payment

There are a handful of creative ways that homeowners can slowly pay down the principal amount and start saving on interest. One quick and effortless way of paying off mortgage early is by rounding up your monthly payment.

Every month when it is time to make a payment...round up to the nearest hundred!

You may think, simply adding such a small amount won't make a difference. But it does! If you do this consistently, every month, you can pay down hundreds of dollars off of the principal every year.

Example:

| Current Monthly Mortgage: | $1,024 |

| Round Up to Nearest Hundred: | $1,100 |

| Difference Applied to Principal: | $76 |

Over time the money will drastically add up. Take a look at how much extra you will be adding towards the principal amount.

| Total Over 1 Year: | $912 |

| Total Over 5 Years: | $4,560 |

| Total Over 10 Years: | $9,120 |

You will notice that if you round up to the nearest hundred consistently over the year, physiologically it will become more and more natural. It will begin to feel like your original payment. Also, having an even number will make it easier to calculate your monthly budget.

2. Bonuses and Tax Returns

Did you just recently get a bonus at work? Consider applying a portion of your bonus to your next payment. This may not be exactly what you want to spend your bonus on…but you have to be committed to tackling the debt to really see the true compound effect over time.

Combine this effort with the first tip mentioned and you will really start to see the needle move. Just remember that anytime you are making any extra payments to your mortgage, always apply it towards the principal.

If you have any questions, always reach out to your mortgage company to verify that it is being applied correctly. The last thing you want to do is pay extra on your monthly payment and find out that it was applied towards the interest.

3. Bi-Weekly Mortgage Payments

A bi-weekly payment is when you make a one-half payment every other week vs paying one full payment once a month. Some companies offer bi-weekly payment services which may not be necessary. Depending on your loan, there may be restrictions. It is always good to know the guidelines for your loan so they are followed correctly.

How does bi-weekly actually work?

Each calendar year is made up of 52 weeks. If you make a half-payment every other week that equals to 26 half payments at the end of the year. Which is equal to 13 full payments. Adding one extra payment a year. This is just another way homeowners are paying down their mortgage faster.

One of the most important things to remember when deciding to pay off your mortgage early is to be 100% dedicated and consistent.

4. One Extra Payment

Making one full extra payment every year may be a more difficult approach when it comes to paying off your home early. Some homeowners may find it harder to shell out such a large amount at once. But for some...this may be an option.

Making one full extra payment every year may be a more difficult approach when it comes to paying off your home early. Some homeowners may find it harder to shell out such a large amount at once. But for some...this may be an option.

There are a handful of ways that you can do this where you don't necessarily pull the full amount directly from your saving account or emergency fund. Consider going through your belongings and getting rid of old clutter that you may not need any longer and selling it in a yard sale.

By getting rid of these older items you not only declutter and regain lost square footage, it is a great way to make a little bit of extra money.

5. Add 1/12th Monthly Payment

When learning different ways to pay off mortgage early, this may be one of the easier ways to add that one additional payment every year. Since you are breaking up the thirteenth payment up into twelve, much smaller payments and applying it towards principal every month. This will more than likely have the smallest dent on your monthly expenses but will still achieve the same results at the end of the year.

Below is a breakdown on how you can divide that 13th payment by twelve and apply that amount to your payment every month.

For an example:

| Monthly Payment: | $1,200 |

| $1,200 ÷ 12 mo. | $100 |

| New Payment: | $1300 |

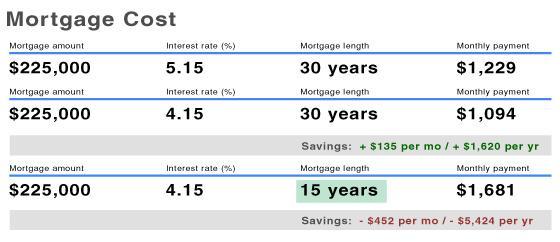

6. Refinance

If you have a higher interest, one way to reduce your monthly payment is by refinancing. One common rule of thumb is that if you can save at least one percent off of your current mortgage, it may make sense for you to refinance.

Considering the cost of closing on a loan and how long you decide to stay in the Louisville home-refinancing may be the right move.

Look at the table as an example. If your current interest rate is 5.15% and you could refinance at 4.15%. You could possibly save around $135 per month and $1,620 throughout the year. That is a huge saving! Also in the example, you will see the length of the loan reduced to 15 years vs a 30-year loan. Your monthly payment, of course, is going to be higher. A $452 per month increase but you will pay off your home 15 years sooner and also save over $90,000 in interest.

7. Shorten the Loan

As mentioned in the previous tip, if you refinance your home you can either reduce your monthly payment or even better...you can reduce the length of your loan. Depending on what mortgage option is best for you. Some homeowners are deciding on obtaining either a 20-year loan or even a 15-year loan vs having a traditional 30-year loan.

Chances are if you shorten a traditional 30-year loan down to a 15-year loan, your monthly payment will increase. If you have a higher interest rate, now may be a good time to not only refinance and save but to also consider shortening the length of the loan. The monthly payment may not increase too much and you could save thousands of dollars in interest.

Conclusion to Paying off Mortgage Early

These are many different approaches to how people are getting creative and paying off their mortgage early. Surprisingly enough there have been reports in the past that note that nearly 30% of homes in the US are owned ‘free and clear’. This is very promising to first time homebuyers who are wanting the achieve financial freedom and eliminate all their personal debt.

Posted by Nathan Garrett on

Leave A Comment